What kind of bubble is AI?

The dot com bubble is a helpful analogy, but not the most precise one

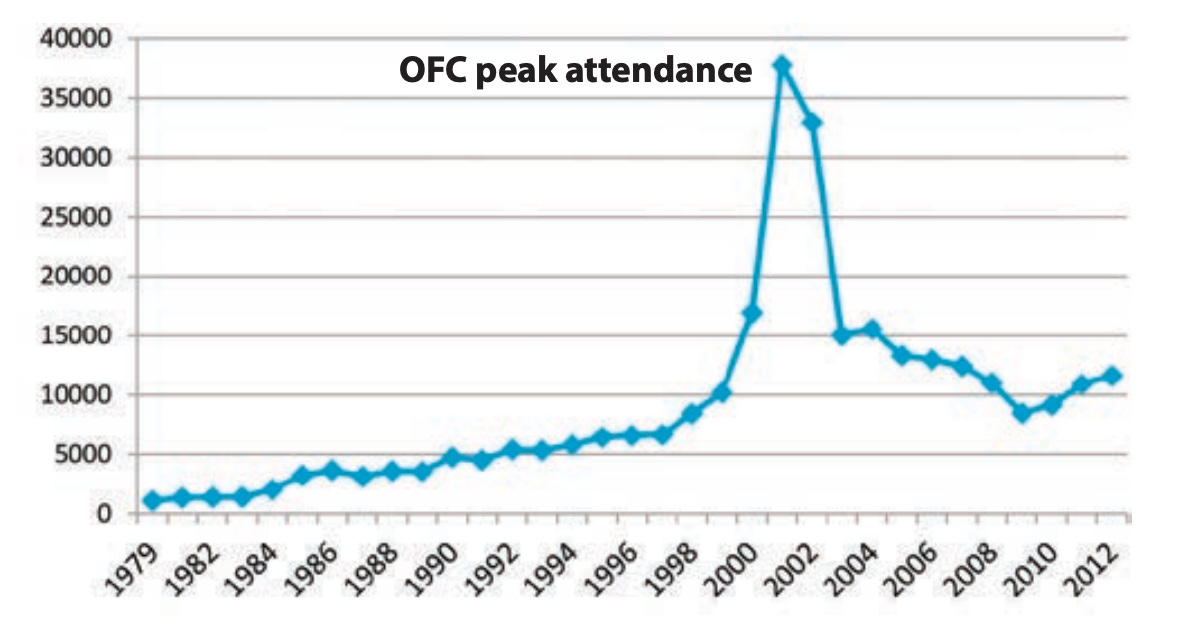

Most of us can look at a graph and know when it shows a bubble. And that’s the case for this chunky JPEG-artifacted graph, right here.

You don’t need to know what OFC is, or peak attendance, to guess that the blue line’s crest is the puffing of a truly epic bubble before an equally epic pop. And as your eyes descend to the timeline, it becomes clear that the bubble is the dot com bubble.

Except, it isn’t.

Well, not exactly.

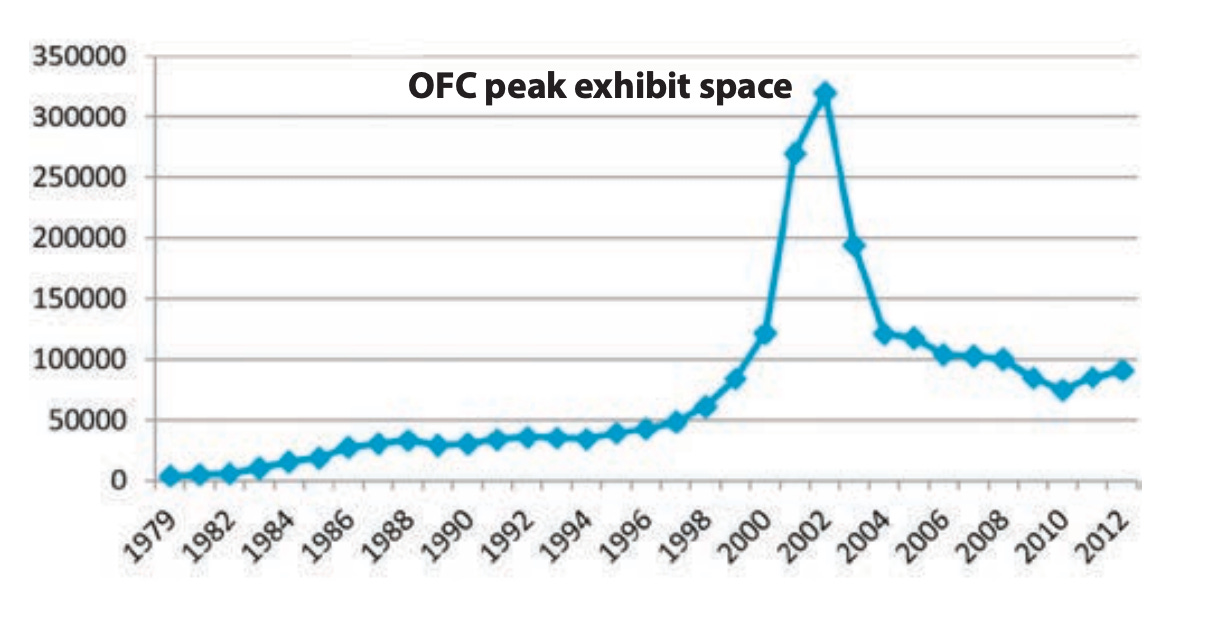

“OFC peak attendance” is the label of this chart, and the chart is paired with a chart of “OFC exhibit space,” which follows a nearly identical arc.

OFC, in both cases, represents the Optical Fiber Communication conference, and it comes from their retrospective on a narrow slice of the dot com bubble: the fiber bubble. These are the people who covered the United States with fiber optic cable in the late 90s.

Discussions of the current AI bubble mistily recall the dot com bubble of the late ‘90s and early 2000s, and AI-skeptics are likely to invoke famous dot com failures like Webvan, an early online grocery delivery company, or Pets.com, the other iconic example of early internet enthusiasms that failed to survive the dot com crash.

That analogy isn’t precise. There is an AI bubble, but it’s probably better represented by a large crop of AI wrappers: companies that plug into leading AI companies, like Anthropic or OpenAI, and sell their own integration of those leaders’ software. Imagine an “AI workout app” that has some nice branding, but basically sends preprogrammed instructions off to OpenAI for one of their GPT models to do the real work. The recent crop of small startups is littered with companies like this, and these provide a neat analog to the 2000s web bubble, since both groups include consumer-facing enterprises with unproven models.

But just because some consumer AI startups might be bubbly in their lack of revenue, that doesn’t mean AI as a category is a bubble. Anthropic has a $47 billion run rate revenue, and while that doesn’t indicate anything about their profitability, it does indicate massive real interest in their product. This is a big deal! The specific businesses in AI are deeply uncertain, but people want AI in the same way they really wanted fiber optic cable.

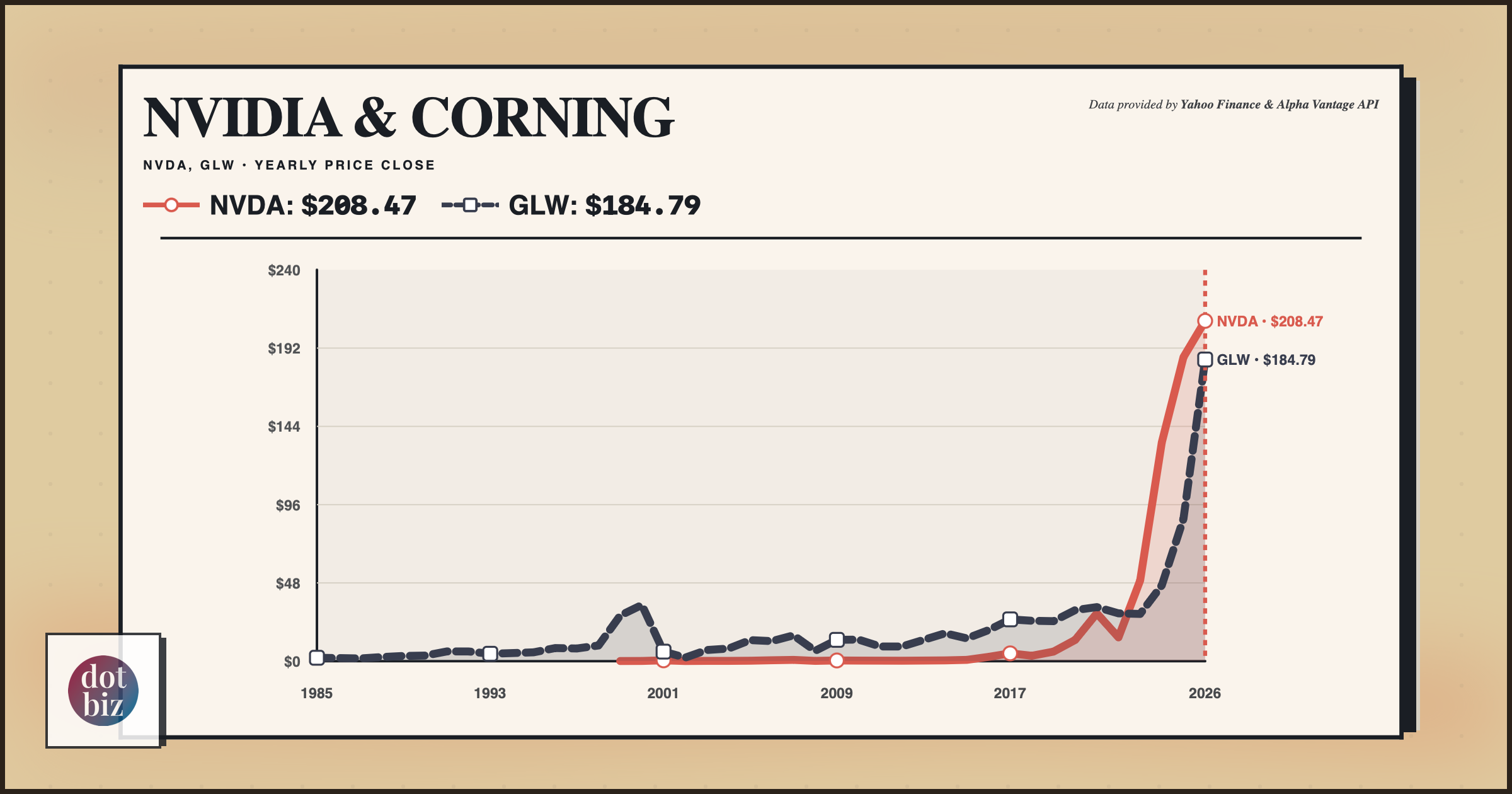

This dynamic is clear if you look at the stock price of Corning and Nvidia. The famous glassmaker makes optical fiber, and their stock price tracks the waxing and waning of fiber enthusiasm even better than attendance charts for a fiber-optic convention. They also benefit from a boom in AI, because their fiber supplies new data centers. NVidia, meanwhile, is mostly a modern phenomenon, since it was traded as a gaming company before its GPUs were used in the crypto boom and then AI. See how Corning has a pop in 1999, before roughly tracking NVidia’s rise (in price, not market cap)?

The fiber optic bubble was a real bubble. Companies over-invested in fiber and bankruptcies followed. But the interest and enduring value was real value that we still benefit from today. Infrastructure buildout done in the late 90s has meaningful implications today, but there were still big losers when the bubble burst.

The AI bubble is not a bubble like the consumer companies of the initial dot com frenzy — it’s a massive infrastructure boom, like fiber, with lots of possible bubbles that could pop. Like the fiber boom, or even the railroad boom a century before that, this might be frustrating because it makes it harder to invest around. But it does have the takeaway that AI shouldn’t be ignored, because the demand is real.